INSIDE CASHLINK

Investor protection within Cashlink’s digital company share

Startups are fast-growing companies with business ideas that have the potential to shape whole industries. Especially in the early days startups need a lot of capital to finance their growth. To do so, they sell shares in the company to investors who believe in their mission and in the economic success of the mission. If the company is sold or makes money, investors receive a part of that according to the percentage of shares they hold.

We at Cashlink have issued a security representing a share in the company. The security grants it’s owner the same economic rights as a shareholder who is registered with the commercial register. To issue the security we have developed a Blockchain-based technology that reduces the costs of security issuance dramatically. Therefore such digital securities become a new option for startup’s growth financing needs. Financing rounds become completely digital and international.

Growth can require a startup to sell shares in several rounds. The more investors the startups include in their shareholder base, the larger the company’s share capital will be. When this happens, investors from the very beginning have to fear that their percentage of the share capital will become smaller. In order to protect themselves against this, many investors rely on contractual rules against the dilution of their shares. Such contractual rules are important to build trust during the deal process.

Let’s look at an example to examine more closely how such contractual rules function in theory:

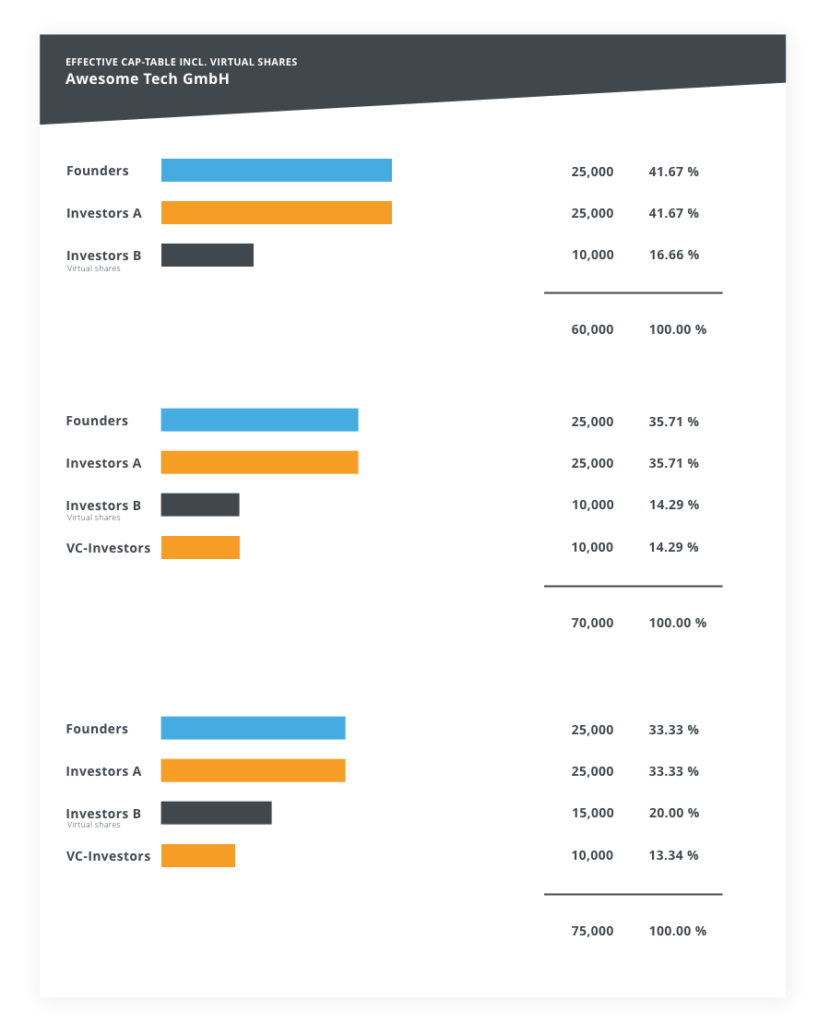

- To start with the company has 25,000 shares all owned by the company’s founders.

- In a first funding round the company issued 12,500 new shares to a group of investors (Investors A). The founders then owned 66.67 % and Investors A owned 33.33 %.

- Then sometime later, they sold another 12,500 shares to a group of investors (Investors B). If there were no contractual rules in place, the founders would own 50 %, Investors A would own 25 % and Investors B would own another 25 %. The shares of investors A were diluted.

- However, Investors A have set a rule which protects them from reducing their share. To secure the 33.33 % share of Investors A, the company now has the obligation to issue another 6,250 shares to Investor A without payment. The founders now own 44.45 %, Investors A still owns 33.33 % and Investors B hold 22.22 %.

Down round protection mechanism for early investors within venture capital funding rounds.

Of course, the founders would only commit to such an obligation, if the valuation of the company decreases from the first to the second financing round. If the valuation increases it’s a good deal for everyone to issue more shares even if the percentage of shares decreases.

Such rules work very well for investors that own real shares. But what about investors that own digital shares? Their digital securities have the same economic rights as real shares and their value would, therefore, be diluted in the same way. To provide the same protection to these investors we implemented a similar mechanism for the digital shares:

Investor protection in case the company sells cheap shares

Down round protection mechanisms all base on the idea that if a company sells shares for a price below a certain threshold, the existing investors get compensated with new shares without payment. If you own digital shares that would mean that you receive more digital securities without actually paying for it. As the creation of new digital shares could lead to complex scenarios in secondary markets we decided on another way to do it.

Instead of creating new digital shares the issuer has the possibility and the obligation to maintain a so-called calculation factor securely stored on the blockchain. The calculation factor determines how many digital shares equal one real share. In a case where an investor would receive more digital shares, the issuer simply decreases the calculation factor which in turn leads to a higher value per digital share. To explore how this mechanism works, let’s consider an example:

The company has 50,000 real shares registered with the commercial register. In addition, there are 1,000,000 digital shares that can be bought by investors. The calculation factor at the time is 100, so 100 virtual shares equal 1 real share. That, in turn, means that these digital shares are worth 10,000 real shares.

- Let’s assume that the company has sold all digital shares to investors for a price of EUR 5.00 per digital share. The price of a real share then was EUR 5.00 * 100 = EUR 500 and the company has got a post-money valuation of EUR 500 * (50,000 + 10,000) = EUR 30,000,000. The total value of the digital shares is now EUR 500 * 10,000 = EUR 5,000,000.

- Now the company makes a venture capital round using the commercial register and issues 10,000 real shares for a price of EUR 100. That result in a post-money valuation of EUR 100 * (10,000 + 10,000 + 50,000) = EUR 7,000,000. That means that the digital shares are diluted because the total value of the digital shares is now EUR 100 * 10,000 = EUR 1,000,000.

To protect digital share investors from such a dilution the issuer has set a minimum price which is called “Down round protection price” during the setup of the digital security. If the company sells real shares below this threshold, the digital share investors are compensated. Let’s do the example above including the protection mechanism with a down round protection price of EUR 200. What now happens is the following:

- We calculate a new guaranteed price per share using the weighted average method: ((10,000 * EUR 200) +(10,000 * EUR 100))/(10,000 + 10,000) = (2,000,000 + 1,000,000) / 20,000 = EUR 150.00

- It is the obligation of the company to guarantee that the issued virtual shares are worth EUR 150.00 per share. However, the price per share for the newly issued shares is EUR 100. To adjust the value of the digital shares the calculation factor is updated to be 100 * EUR 100/ EUR 150 = 66.67.

- The 1,000,000 issued digital shares are now worth 1,000,000 / 66,67 = 15,000 real shares. The total value of the digital shares is now EUR 100 * 15,000 = EUR 1,500,000.

Down round protection for digital company share investors.

Investor protection if the company sells cheap digital shares

The rule above protects investors if the company has to sell cheap real shares. But what if the company sells cheap digital shares? How much investors get paid out is determined by the percentage of digital shares they own. The more digital shares issued the lower is the percentage of digital shares for the investor. Again, this would mean a dilution that is only accepted by investors if the valuation of the company increases. However, consider an example with two digital share investors (Investor A and Investor B). Investor A buys digital shares for a certain price and then Investor B buys digital shares for a lower price:

The company has 50,000 real shares registered with the commercial register. In addition, there are 1,000,000 digital shares that can be purchased by investors and 100 digital shares equal 1 real share:

- Investor A buys 100,000 digital shares for a price of EUR 5.00 per virtual share. Their share is then (100,000 / 100)/((100,000 / 100) + 50,000) = 1/51, the valuation of the company after the digital shares are sold is EUR 500,000 / (1/51) = EUR 25,500,000.

- Investor B buys an additional amount of 100,000 digital shares for EUR 1.00 per digital share. That is an investment of EUR 100,000 and a post money valuation of EUR 100,000/(1,000 / (1,000 + 51,000)) = EUR 5,200,000.

- The value of the digital shares in possession of Investor A is then 1/52 * EUR 5,200,000 = EUR 100,000.

To protect the investor from such a decrease in value, there is a minimum price per digital share. The issuer is not allowed to sell digital shares below this threshold. Thus, this is a guarantee for a minimum valuation the company must achieve by selling digital shares.

Bringing these mechanisms on-chain

For now, these mechanisms need the active participation of the issuer. It is the legal responsibility for the issuer to not sell digital shares below the anti-dilution protection price as well as to update the calculation factor on the blockchain if a down round has been conducted. Although these tasks are legal responsibility for the issuer, investors need a certain amount of trust that these things won’t become an issue after investing.

We are certain that this is just the beginning of blockchain adoption. In the future, we will have stable coins, cross-blockchain compatibility and even commercial registers that are based on blockchain technology. Using these enhancements it is possible to enforce both protection mechanisms directly on the blockchain. Such a trust-enhancing and fully digital process will effectively remove costs and uncertainties for investors as well as startups.

If you have any questions regarding these mechanisms or the design of the shares as digital securities in general feel free to contact us!

Talk to our team of experts

Our team will be happy to advise you. Arrange a free consultation now.

Simon Censkowsky

Head of Business Development

s.censkowsky@cashlink.de

linkedin.com/in/scenskowsky