Crypto Securities Explained

Get started with crypto securities now

The most important information on the issuance of crypto securities at a glance. Take advantage of the opportunities offered by the eWpG now.

Study

More than 50% of all clients plan to issue crypto securities

On June 10, 2021, the law on electronic securities (electronic Securities Act, or eWpG in short) came into force. This will make the purely digital issuance of securities possible for the first time (including crypto securities). As we at Cashlink have been eagerly awaiting this regulatory change, we were curious to see how the market perceives this new law. We came to the conclusion that more than 50% of our clients showed interest in crypto securities and their use cases. But what are the exact advantages of crypto securities? Compared to traditional securities, tokenization gives you:

65% lower costs

compared to traditional securities, as the costs of the value chain are drastically reduced.

24/7 transferability

Previously illiquid assets can now be transferred easily around the clock anywhere in the world.

99% faster processing

faster settlement of processes, as the speed of transactions is significantly increased by the use of tokenized securities.

100% more transparency

because transactions are stored in an unchangeable and transparent manner. This strengthens trust between market participants.

And what exactly are the differences of crypto securities compared to security tokens?

In our whitepaper, we answer this question and more. As the topic of electronic securities is still relatively new, we would like to use this whitepaper to create a general understanding of this topic and present various use cases. Click here to get your free whitepaper (In cooperation with Annerton).

- STOs & Crypto Securities: The Comparison

- Opportunities through crypto securities.

- The four most important terms concisely summarized

- The law in detail: What to consider?

- Advice for the personal crypto security

Timeline

The path to today's law

The last three milestones for the Electronic Securities Act (eWpG)

- May 6, 2021

Adoption

The Bundestag passes the new Electronic Securities Act (eWpG).

- June 9, 2021

Annunciation

The Electronic Securities Act (eWpG) is announced in the Bundesgesetzblatt.

- June 10, 2021

Becomes effective

The new Electronic Securities Act (eWpG) officially comes into force.

However, the detachment of the deed obligation is already an ongoing topic since 2019

March 2019

The BMF and the BMJV have published a key issues paper for the regulatory treatment of electronic securities.

September 2019

The German government adopts its blockchain strategy, with the aim of promoting digital innovation in Germany.

August 2020

The first joint draft bill for the Electronic Securities Act (eWpG) is published by the BMF and BMJV.

December 2020

The first draft of a law on the introduction of electronic securities is finished.

"We feel that the launch of crypto securities was the right first step to digitize and decentralize classic capital market processes. It brings us closer to our vision of a DLT-based capital market and was a tremendous validation for us on the work we've already done."

Solutions

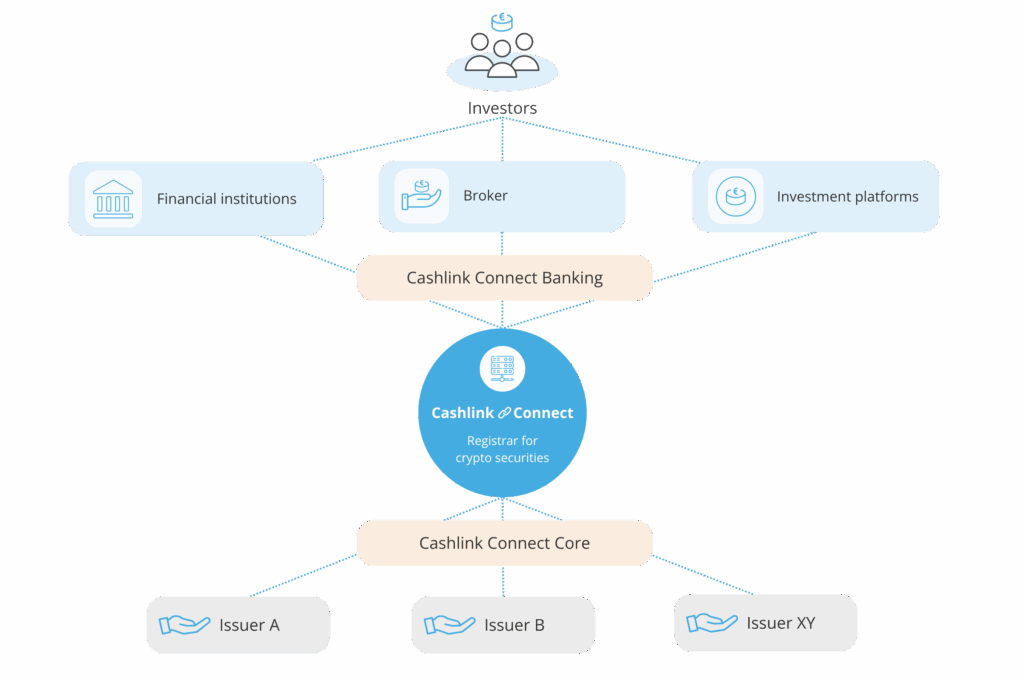

How Cashlink enables token-based Capital Markets

Cashlink provides a modular solution along the issuance- and post trade valuechain of token-based securities. As a regulated financial institution after the German Banking Act (KWG), Cashlink holds a license as a crypto securities registrar and qualifed crypto custodian.

Cashlink Connect Core

The issuance module enables issuers to issue regulatory–eWpG-compliant, token-based securities on the blockchain — with a proven and multiple times audited smart contract suite. Cashlink’s robust and scalable API based infrastructure, connects issuers with brokers and trading venues and is interoperable with stablecoins and upcoming ECB Digital Money solutions.

Cashlink Connect Banking

The settlement module enables custodian banks, brokers and exchanges to seamlessly settle token-based securities post-trade in full regulatory compliance in collective entry. Get access to all token-based securities registered by Cashlink and ensure secure, efficient, and transparent settlement on the blockchain without added complexity.

Definition

Crypto Securities

Comparison

Crypto securities vs. security tokens

Crypto securities | Security token | |

|---|---|---|

| Liability | The crypto securities registrar shall be liable within the scope of regulated activities | Issuers are liable for the issuance. The secondary market is not covered here |

| Transferability | The transfer always takes place via the register and is regulated | The transfer is strongly dependent on how the token is designed |

| Transparency | Everything in the register is valid and transparent to the public | There is little publicly available information. Only WIB and prospectus |

| Good-faith protection |  |  |

| Liability in case of insolvency | Priority, subordinate | Subordinate |

| Suitability for institutional investors | | |

Definition

Crypto securities registry

eWpG-FAQ

Frequently asked Questions about the eWpG

Will security tokens now be replaced by electronic securities?

Will physical global certificates be completely replaced?

When do electronic securities legally come into existence?

Who is the holder and who is the beneficiary?

These two points are clearly defined in the law. The holder is the person who is entered as the owner in the electronic securities register, while the beneficiary is the person who holds the right arising from a security.

Who can be entered as a holder in the electronic securities register depends on whether a collective entry or an individual entry is to be made:

In the case of a collective entry (electronic counterpart to securities evidenced by individual or collective certificates held in collective custody), a securities clearing and deposit bank (custodian) is the registered holder of electronic securities. In this case, therefore, the formal holders are not the same as holders of rights (material beneficiaries), unless the electronic securities are the own holdings of the collective securities depository or custodian bank registered as the holder. In order to carry out a collective registration with crypto securities nevertheless, there is the omnibus wallet solution. Here, there are several investors behind a token, which in turn are managed by a custodian. With the custodian, it is important that a custodian license is available.

In the case of a single registration, any natural person or legal entity, or partnership with legal capacity, can be the holder of the electronic securities. Unlike in the case of a collective registration, the (formal) holder is regularly also the (material) beneficiary of the electronic security (personal union).

Is the law already fully developed?

Yes, but it is worded “openly” in several respects. The government draft is clearly intended to preserve the current status quo, but also to create new opportunities. The aim is to be able to take advantage of the benefits of electronic securities without major conversion effort. To this end, the new regulations to be created should fit as smoothly as possible into existing civil and supervisory law. In particular, the use of electronic securities will not be “prescribed,” but rather offered as an option.

Those who do not make use of it can issue securities in the usual way using the established and well-functioning process. Those who do make use of it, however, can be assured of the continued validity of previous, highly developed legal principles through the applicability of property law, and thus have extensive legal certainty when entering the new terrain. Furthermore, the aim is to anticipate the market as little as possible, i.e. merely to create a certain framework in which the market can develop. This is done against the background that both the market and the technology are still in the development stage, despite all the progress that has been made.

The legislative materials also show that further digitization is at least being considered by the legislature. In the course of its deliberations on the eWpG, for example, the German government was expressly called upon to evaluate the new regulations after just three years and to make proposals for regulations on the introduction of electronic shares at the beginning of the next legislative period.

Talk to our experts

Our team will be happy to advise you, arrange a non-binding consultation now.

Simon Censkowsky

Head of Business Development

s.censkowsky@cashlink.de

linkedin.com/in/scenskowsky